Battery Energy Storage Systems (BESS) are playing a critical role in today’s grid, offering unmatched flexibility in balancing supply and demand. But turning that flexibility into profit — without degrading the asset — remains a complex challenge.

In a recent webinar with energy professionals across the industry, I walked through some of the key considerations for optimizing battery trading strategies. What follows are a few takeaways I think every battery operator should be thinking about.

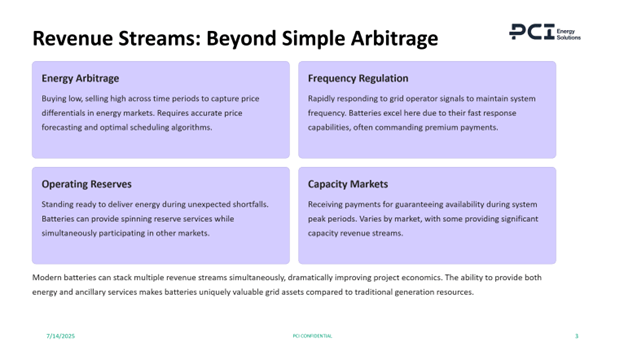

The revenue puzzle: arbitrage is just the beginning

Energy arbitrage (charging low and discharging high) is usually the entry point into market participation. But it’s only one of several revenue streams batteries can tap into. Frequency regulation, spinning reserves, and capacity markets offer additional opportunities to monetize a BESS asset, especially in ISO/RTO markets like CAISO, MISO, and ERCOT.

Modern batteries are uniquely positioned to stack these revenue streams. The trick is co-optimizing participation across them without violating operational limits or shortening the battery’s lifespan.

What’s holding battery operators back?

In my conversations with operators, four challenges come up repeatedly:

- Price forecast uncertainty: Inaccurate forecasts can lead to missed opportunities — or worse, money-losing dispatch decisions

- State of charge (SOC) management: Maintaining charge within safe and contractually compliant ranges is essential for long-term performance

- Revenue stacking complexity: It’s hard to optimize bids across multiple products manually, especially when they compete for the same MWs

- Lack of automation: Many operators still rely on spreadsheets, which don’t scale across assets or adapt well to real-time market shifts

These limitations often lead to conservative, underperforming trading strategies — even when the theoretical potential of the asset is much higher.

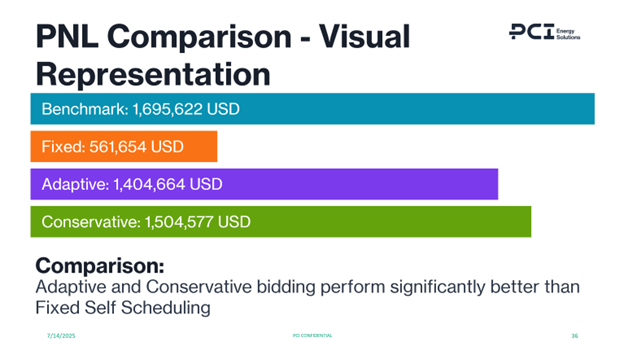

Modeling the gap between theory and reality

Let’s say you had perfect foresight into market prices. What’s the maximum revenue your battery could have made?

That’s the benchmark we used in a recent analysis of a 10MW/20MWh battery operating in a U.S. ISO market. The theoretical maximum, based on actual prices, was over $1.6 million across 13 months. Here’s how three different strategies performed against that benchmark:

- Fixed self-scheduling: ~33% of the benchmark

- Adaptive self-scheduling: ~83%

- Conservative bidding strategy: ~89%

Each step up involved more dynamic use of market data — especially price forecasts — and more automation in adjusting bid curves.

Tools that make this possible

Reaching those higher percentages isn’t feasible with spreadsheets. It requires tools that can:

- Generate AI-powered price forecasts across DA and RT markets

- Automatically co-optimize between energy and ancillary services

- Adjust offers in real time based on market changes and telemetry

- Backtest trading strategies to assess risk/reward profiles before committing

That’s the foundation we built into PCI BatteryTrader, a platform designed specifically to help storage operators scale, automate, and optimize battery participation in ISO/RTO markets.

Want to see the full strategy breakdown?

This post only scratches the surface. In our recent session, I walked through how each strategy works, including the assumptions, modeling framework, and KPI comparisons behind them.

Request to watch our on-demand webinar to see a demo of how BatteryTrader works in real-world scenarios.