We live in a world of pushing and shoving.

Lots of screaming and not much listening and considering.

The formerly staid energy industry is suddenly confronted with a double dose of technological change and binary thinking on the energy transition.

This blog post will cover how a utility manages legacy resources in a dynamically changing portfolio. I will address three basic pragmatic principles while discussing the future of natural gas, market volatility, and new load patterns.

Basic pragmatic acknowledgements

If you want to examine the future of managing your legacy resources in a world shunning fossil fuel and nuclear resources and embracing renewable energy and storage, you need to begin by acknowledging three simple facts:

- More people use more energy.

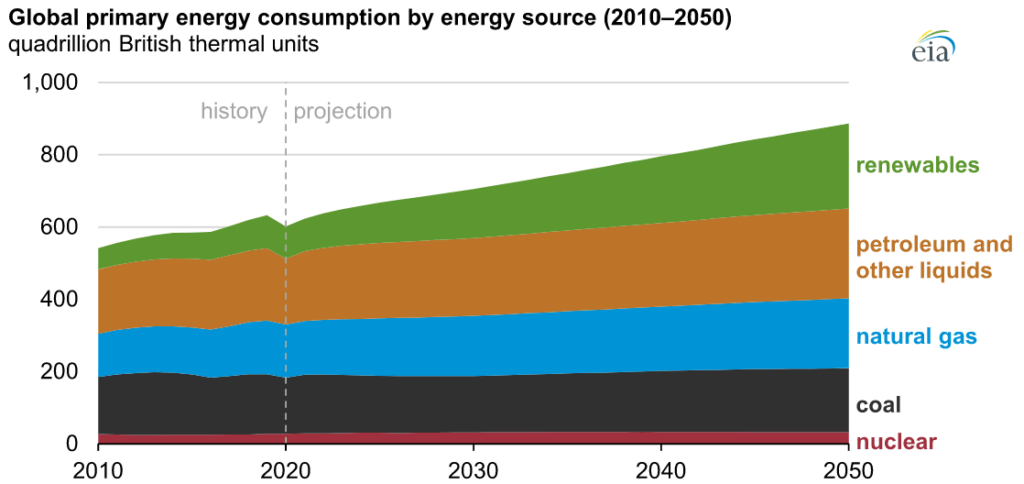

With the global population expected to increase by 2 billion in the next two decades, electricity consumption is estimated to increase by almost 49% by 2040.

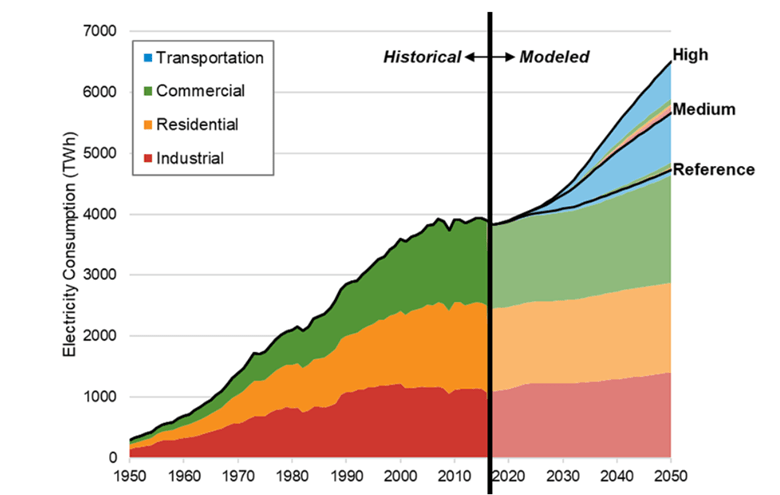

2. Electrification will substantially increase energy demand.

In 2018, NREL Electrifications Future Study forecasted that the “electrification of everything” could increase U.S. electricity consumption by nearly 40% by the midcentury.

3. Electricity does not come from the wall.

Unless we plan to return to the “Little House on the Prairie” days, renewable energy coupled with storage will clearly not be nearly enough to serve load reliably and affordably.

So, what does it all mean?

- Legacy resources will remain, and we will need more natural gas, not less.

- Volatility will persist due to geopolitical issues as well as domestic supply constraints.

- Understanding new load patterns will be extremely critical.

Here to stay

Despite the populist rhetoric today coupled with grandiose goals of 100% renewable energy by 2050, pragmatic electrical engineers keeping our electrical grid functioning know differently.

What is also true, however, is that the currently hostile regulatory attitude toward legacy resources will not likely change anytime.

So natural gas pipeline construction will continue to be severely challenged, along with adding natural gas combined cycles to integrated resource plans.

As for coal, the last new coal plant in the United States has been built.

Take that to the bank.

Do you remember the last time a fossil fuel plant closed because it was too old to make electricity? Neither can I. Plant retirements happen due to economics. I expect market model changes to focus on reliability and financially rewarding generators who perform when needed most and who can best complement the continued onslaught of intermittent wind and solar resources.

At the end of the day, natural gas is the only and best resource to handle the volatile swings in solar and wind generation. Coal and nuclear can’t porpoise when producing megawatts. You can’t drive a dump truck like a Ferrari.

When Charles Dickens wrote, “It was the best of times, it was the worst of times,” he could have been speaking of the state of the U.S. natural gas industry. We need natural gas more than ever to meet challenging carbon reduction goals via the addition of wind and solar. Still, we will make it as difficult as possible by making the creation of new pipelines nearly impossible.

Two things happen when you tell an industry you need them badly for the next ten years, but then you want them gone. First, who would commit to large-scale capital expenditure projects in that environment? Who would lend them money to do so?

Optimizing and navigating through the complexities of your pipeline will be critical. The bottom line is that the U.S. will be expected to produce substantial natural gas to feed the U.S. and Europe via liquified natural gas (LNG) while not having many additional pipelines available.

And we will thus continue to struggle to deliver natural gas to known constraints like the West Coast and New England.

The best of times and the worst of times indeed.

Price volatility

The impact of the Russia-Ukraine war was felt quickly and violently in the natural gas market in Europe and the United States.

Chart used with permission from Trading Economics.

Eliminating a third of the global oil and gas supply introduced a price shock and a new reality. European storage levels and the importance of LNG to replace Russian supplies now impact natural gas prices on a global level. Why do we now follow the status of the Freeport LNG terminal daily? So we can find out if the 2.1 billion cubic feet of gas the terminal can process will be shipped to Europe, reduce U.S. supply and be bullish for U.S. natural gas prices or whether that gas remains stranded in the U.S., increases supply, and is bearish for U.S. gas prices.

It’s a small world, after all.

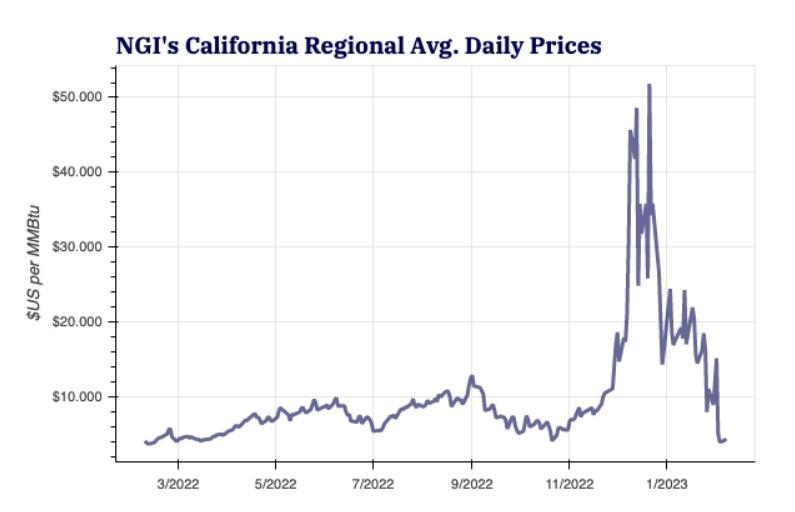

But Europe is not the only reason for volatility. Known U.S. natural gas supply and transportation constraints recently caused prices to soar on the West Coast.

Source: Natural Gas Intelligence (NGI)

Extreme weather plus reduced supply plus increased demand equals continued volatility.

Barring some federal action impacting natural gas prices directly or restricting exports overseas, the $2-$3 natural gas era is over.

Managing your price volatility via prudent hedging strategies will increase complexity and importance. Sometimes selling your gas to a neighbor and buying power cheaper from somewhere else will be the most optimal day-ahead plan.

So optimizing your transmission portfolio will become just as important as optimizing your pipeline contracts.

Residential and commercial load

Your load forecast is the most significant risk to any utility on a day-ahead or long-term basis.

The coincident peak load is a critical factor in rate design and integrated resource planning.

When the coronavirus pandemic first struck, I wrote about some early discoveries of the impact on the load profile. While the final verdict on teleworking has yet to be known or understood, early indications state that the hybrid model seems to be the new normal. However, even the hybrid model introduces complexities and risks to forecasting residential and commercial loads.

How about we add one more log to the load complexity fire? The dawning of the era of the electricity prosumer, formerly known as the consumer.

Electric vehicles, solar panels, batteries, and Nest Learning Thermostats all present a threat and an opportunity for reliable load forecasting.

The digitalization age will present a utility with a unique opportunity to develop a more intimate relationship with the customer regarding understanding and having access to the prosumer data and some level of influence on these distributed energy resources. Failure to develop that relationship will introduce an unacceptable risk to developing accurate load forecasts.

The truth remains that load forecasting will increase in difficulty, and this risk needs to be managed to avoid unacceptable financial risk.

One way to address risks on extreme weather days is to use your battery storage wisely.

While much has been written about the different value streams of lithium-ion utility-scale storage, early results indicate these batteries depredate more than anticipated when they constantly porpoise to manage renewable generation swings.

Peak shaving is where batteries can deliver the biggest ROI buck. If you can forecast the three to four days per year where those three to four hours of that day bring the most risk to your portfolio, you can shave your coincident peak load and save significant money.

Load forecasting will increase in significance, and you are better off building or buying multiple forecasts. AI forecasts sound promising but have yet to be fully developed and proven.

Pragmatism

Managing your legacy resources in a dynamically changing portfolio requires pragmatic planning and courage to communicate directly and honestly with your customers and regulators.

Simple math points to the increased demand for electricity in the coming decades, along with the critical importance of natural gas.

Political realities also dictate that the difficulty of managing these portfolios will increase in complexity as utilities strive to do the near impossible: serve customers as reliable, affordable, and environmentally considerate as possible.

Understanding your natural gas pipeline contracts and constraints, optimizing your transmission portfolio, and improving your knowledge and ability to forecast and influence the behavior of your residential and commercial load has never been more critical.

Harry Truman once said, “There is nothing new in the world except the history you do not know.“

Pragmatic planning requires us to observe the recent lessons in the European and U.S. energy markets as we plan for the future.

We help our customers manage natural gas and coal contracts, transportation and storage with midstream energy software built specifically for physical power market participants. If you’re interested in learning more about how you can manage your legacy resources, visit our Gas & Fuels Management page and take a tour of our gas and coal management system in our software demo.