Utility-scale battery storage in the United States has expanded significantly in recent years, driven by the continued integration of renewable energy resources like wind and solar. In 2025, battery capacity additions are expected to hit a record 18.2 gigawatts (GW), building on the previous year's record of 10.3 GW, according to the U.S. Energy Information Administration (EIA). These batteries will account for 29% of all new installed power capacity. While batteries enhance grid reliability and flexibility, their economic returns depend heavily on well-crafted bidding strategies that account for both market dynamics and operational constraints.

This blog post explores how energy companies can design bidding strategies to optimize profits and manage risk in competitive power markets, such as those operated by Independent System Operators (ISOs) and Regional Transmission Organizations (RTOs).

The economic logic of battery storage

Battery storage systems are characterized by three key parameters: charge holding capacity (measured in megawatt-hours), power rating (megawatts), and round-trip efficiency (the percentage of energy recovered after charging and discharging). Consider a 10-MW, 2-hour battery with 90% efficiency. It can store 20 MWh of energy, takes two hours to fully charge, and loses 10% of input energy in the process.

The core economic principle is simple: buy low and sell high. To break even, a battery must pay no more than 90 cents per kilowatt-hour to charge if it plans to sell that energy at $1 per kilowatt-hour. Batteries can respond almost instantaneously, making them ideal for both price arbitrage and ancillary services that support grid stability.

Arbitrage: Capitalizing on Price Swings

In regions with high renewable penetration, electricity prices can fluctuate wildly due to swings in net demand (demand minus renewable generation). Weather patterns, outages, and bidding behaviors all contribute to these price shifts. During a heatwave in August 2023, for example, real-time prices in ERCOT, the Texas grid operator, surged above $1,000/MWh and reached as high as $5,000/MWh for several hours, while off-peak prices stayed below $100/MWh.

In such scenarios, a 10-MW, 2-hour battery with 90% efficiency that charges during low-price periods and discharges during peaks can achieve substantial returns. For example, charging 22.22 MWh at $100/MWh (total cost: $2,222) and selling 20 MWh at $1,000/MWh (revenue: $20,000), yields a net profit of $17,778.

In such scenarios, a 10-MW, 2-hour battery with 90% efficiency that charges during low-price periods and discharges during peaks can achieve substantial returns. For example, charging 22.22 MWh at $100/MWh (total cost: $2,222) and selling 20 MWh at $1,000/MWh (revenue: $20,000), yields a net profit of $17,778.

Ancillary Services: Monetizing Flexibility

In additional to energy arbitrage, batteries can earn revenue by provding ancillary services like regulation and spinning reserves. These services are essential for maintaining grid stability and reliability. Unlike traditional generators, which must be online to offer reserves, batteries can respond instantly-even while idle—giving them a unique competitive advantage in capturing premiums from high-value ancillary services. Revenues from ancillary services are often essential to justify the high capital investment in battery projects.

Maximizing battery value

Realizing the full economic potential of battery storage requires active participation in ISO/RTO markets, whose complex rules and dynamic conditions make strategic bidding essential. A structured approach includes forecasting, optimization, bid formulation, and performance evaluation. Effective bidding strategies must consider the following key dimensions:

Day-Ahead vs. Real-Time Markets

Day-ahead markets (DAM) involve submitting bids and offers for all hours of the next operating day. Awards are financially binding and most ancillary services are procured through DAM. These markets are generally more liquid and stable than real-time markets (RTM), which clear hourly or even every five minutes and exhibit greater price volatility. While RTMs offer better price arbitrage opportunites, they also pose greater risk if the battery fails to meet its schedule.Energy vs. Ancillary Services

Bidding for ancillary services requires setting aside a portion of the battery’s capacity and maintaining sufficient state of charge. Dispatched energy is settled at real-time prices. Because reserved capacity cannot simultaneously participate in energy arbitrage, operators must weigh the certainty of ancillary service revenues against the potential for arbitrage profits.Self-Schedule vs. Price-Sensitive Bids

Each ISO/RTO has its own battery bidding rules. For instance, CAISO incorporates battery efficiency and state of charge into market clearing, while ERCOT treats bids and offers independently. Operators can either self-schedule—ensuring award certainty but potentially missing price opportunities—or submit price-sensitive bids, which target higher returns but risk not clearing or receiving infeasible awards.

Formuating bidding strategies

Formulating effective bidding strategies for battery storage is challenging in today’s dynamic and complex electricity markets. Prices can be highly volatile, and market rules, especially those governing batteries, can vary widely across ISOs, with some markets lacking battery-specific instruments altogether. To succeed, operators need a structured, data-driven approach built on robust analytics, automation, and adaptability. Our recommended approach unfolds in four steps: (1) forecast day-ahead (DAM), real-time (RTM), and ancillary service prices; (2) formulate multiple strategies using price forecasts and derived optimal battery dispatch; (3) backtest each strategy to evaluate performance; (4) select best bidding strategy based on risk/reward metrics.

Due to lack of perfect foresight, effectiveness must be judged on expected profit and risk exposure—typically measured as the distribution of profit and loss (P&L). In the sections that follow, we demonstrate our approach using a “10-MW 2-hour 90% efficient” battery in ERCOT, focusing exclusively on energy market bidding strategies for simplicity.

Forecast Market Prices For illustration purposes, we elect to use a simple "persistence" model for price forecasting: the forecast of the DAM price is the same as yesterday's DAM published price, and the forecast of the RTM price is the current day DAM published price.

Generate Strategy Variants

- Benchmark: idealized strategy with perfect foresight of the DAM price for DAM bidding. However, perfect foresight of RTM price is available only after DAM bidding is over. This strategy is not feasible in practice but useful for benchmarking.

- Self-Sch: Self-schedule using optimized dispatch based on yesterday’s DAM and today’s DAM prices. The strategy provides operational certainty because the optimized dispatch respects all physical characteristics of the battery.

- Semi-Self-Sch: Self-schedule half the battery's capacity and submit price-based bids and offers for the other half.

- Spread-Price: Bid at 10% below and offer at 10% above the previous day's average DAM prices. Aims to capture wider spreads but increases the risk of partial or infeasible awards.

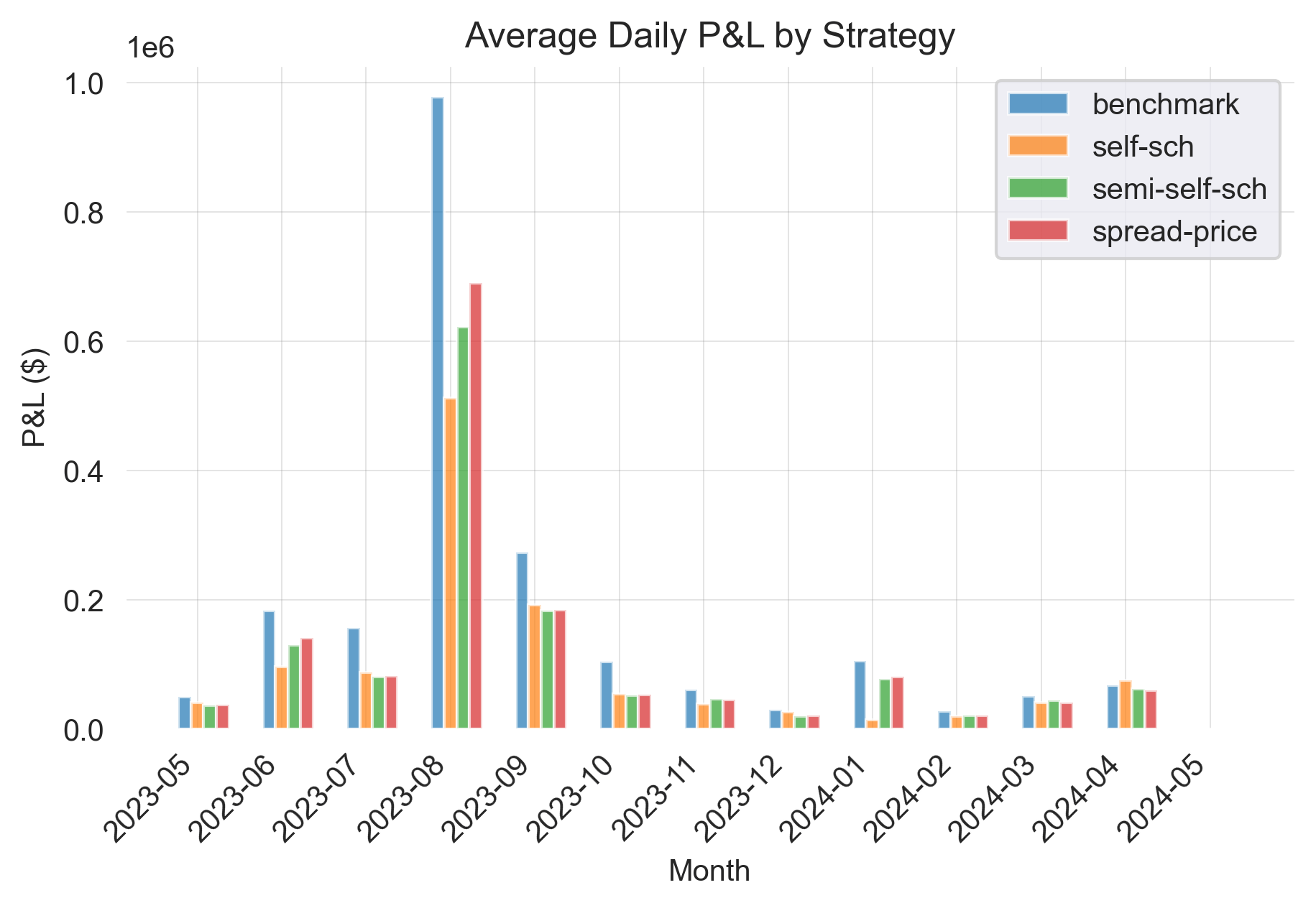

Backtesting Strategies All strategies were evaluated using ERCOT DAM/RTM price data from May 2023 to April 2024. The chart below shows average daily profit/loss (P&L) by month. August 2023 was the most profitable month due to extreme price swings shown eariler.

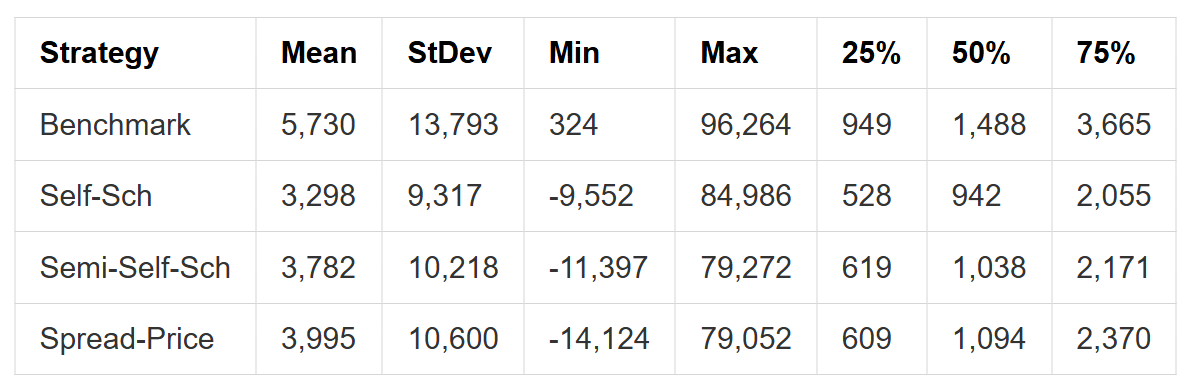

The following table summarizes P&L statistics across the year. As expected, the Benchmark strategy produced the highest mean P&L but the worst 1-day loss.

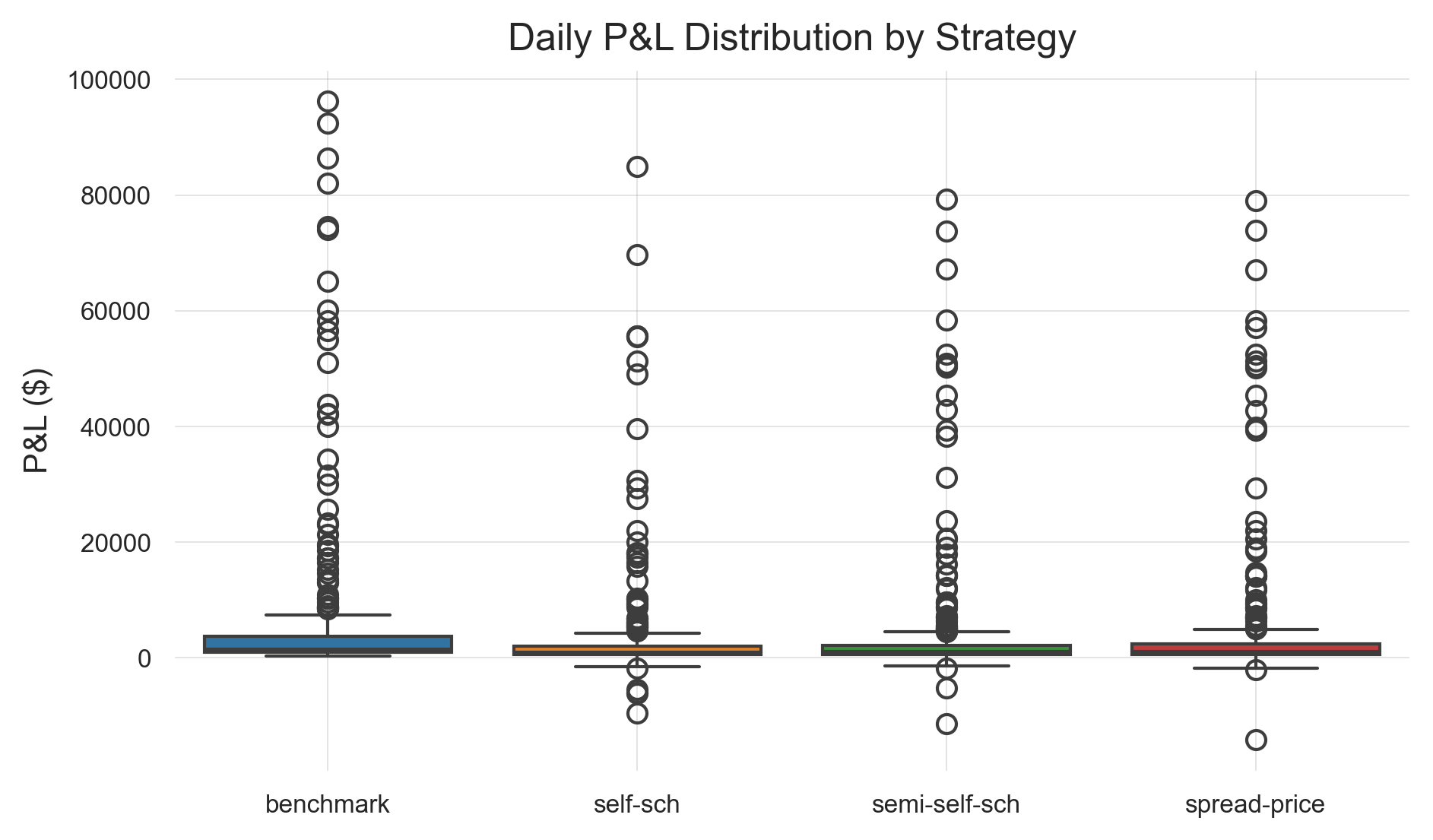

The "Daily P&L Distribution" graph below shows a postive skew, reflecting the battery's value as a "call option" on price spreads. While all strategies delivered positive returns, occasional losses occured due to imperfect forecasts.

Strategy Selection

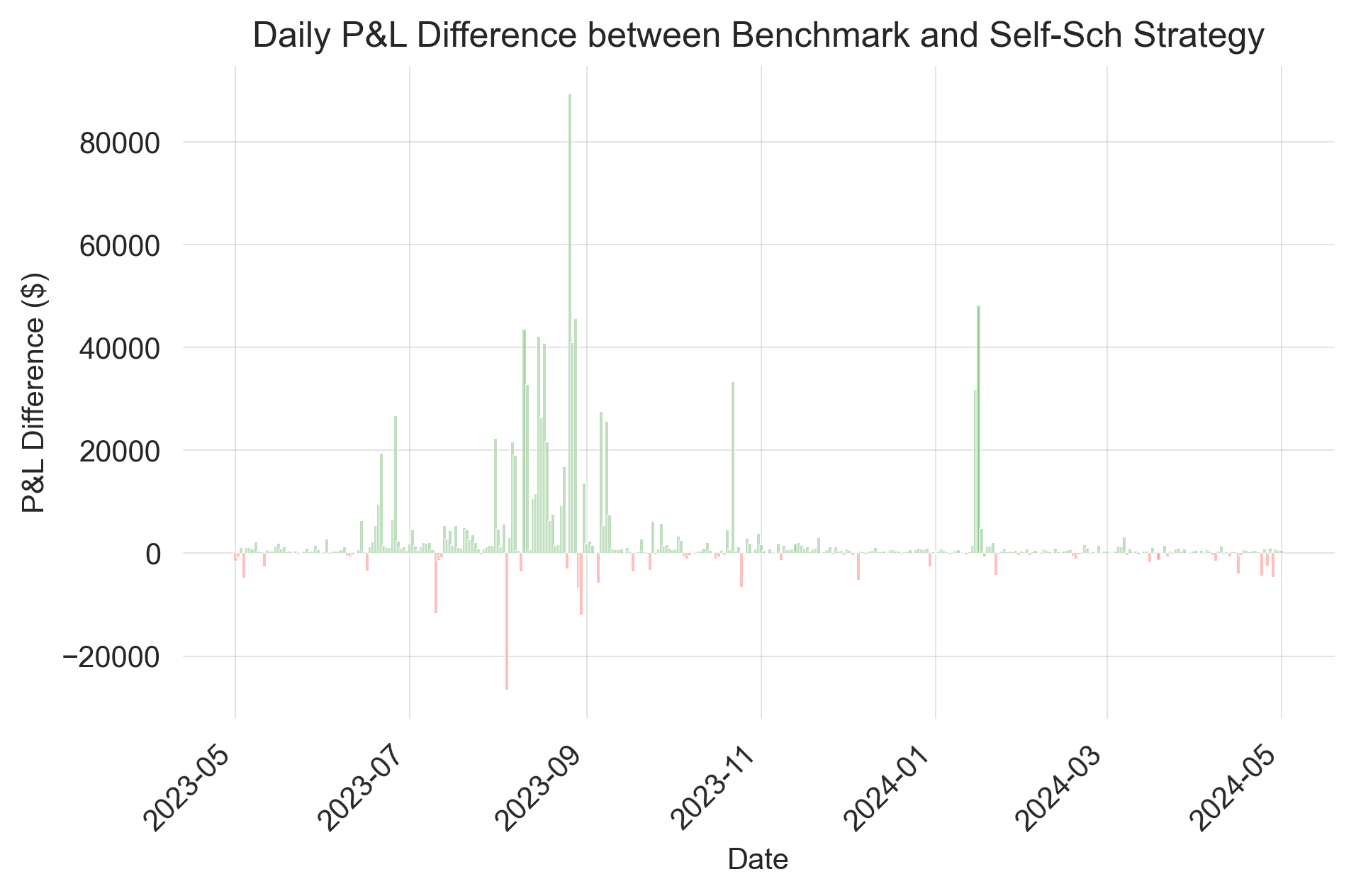

Which strategy is the best? It depends. The Spread-Price strategy yielded the highest expected P&L but also the greatest volatility. The Self-Sch strategy was most conservative, offering lower but more stable returns. Ultimately, selecting a strategy involves balancing profit potential with risk tolerance.Potential Improvements The difference between Benchmark and the other strategies underscores the value of better forecasting. The chart below compares daily P&L between the Benchmark and Self-Sch strategies. Interestingly, Self-Sch occasionally outperformed Benchmark—a result of unanticipated RTM price spikes that weren't captured in DAM forecasts. These cases highligt the importance of evaluating participation in DAM versus RTM and between energy and ancillary markets.

Summary

This illustrative framework emphasizes the importance of accurate price forecasting, structured bid design, and a deep understanding of trade-offs between day-ahead and real-time markets, as well as energy versus ancillary services. Backtesting results confirm that no single strategy is universally optimal—success depends on aligning returns with risk preferences and adapting to evolving market conditions. To maximize battery value, operators must go beyond operational competence and adopt an integrated system of advanced analytics, optimization models, and automation.

Optimize your battery trading strategies with PCI

Our integrated tools—including GenTrader and BatteryTrader—are purpose-built to help you automate forecasting, simulate market scenarios, and execute profitable bidding strategies across ISO/RTO markets. Learn more about our Energy Trading and Optimization solutions.