The Southeast Energy Exchange Market (SEEM) clears every 15 minutes, around the clock, every day of the year. That’s 96 trading sessions per day, 35,040 per year. For each one, a market participant needs to formulate bids and offers that reflect current system conditions and submit them before the window closes.

If you’re doing that manually, you’re not really participating in the market. You’re participating in the intervals where someone has time to look up from everything else they’re doing.

The human-paced ceiling

Manual trading workflows impose a ceiling that has nothing to do with the capabilities of your portfolio. A real-time trader responsible for assembling and submitting bids and offers every 15 minutes is also fielding phone calls, managing exceptions, responding to changing conditions, and doing the rest of their job. In practice, manual participation in a 15-minute market means trading less often, less responsively, and with less precision than the market structure rewards.

This isn’t a criticism of the people running those workflows. It’s a structural problem. The market operates at machine speed. Manual processes operate at human speed. The gap between them is where opportunity goes.

What changes with automation

With autonomous driving, the driver focuses on the destination and route instead of the mechanics of steering. Similarly, autonomous trading lets the trader focus on portfolio positioning and strategy rather than preparing and submitting bids and offers. That model already exists in PCI SEEMTrader, which can formulate bids and offers and submit them automatically. As a result, market participation becomes continuous instead of selective. At each interval, the optimization engine evaluates the portfolio’s capabilities, creates bids and offers based on current conditions, and submits them. After the market clears, the system calculates cost savings and provides real-time P&L feedback, allowing the marketer to review results and respond instead of rushing to prepare the next submission.

This is a different job, and in most cases a better one. The experienced trader’s judgment is applied to decisions that benefit from it, rather than consumed by the mechanics of market participation.

What the data shows

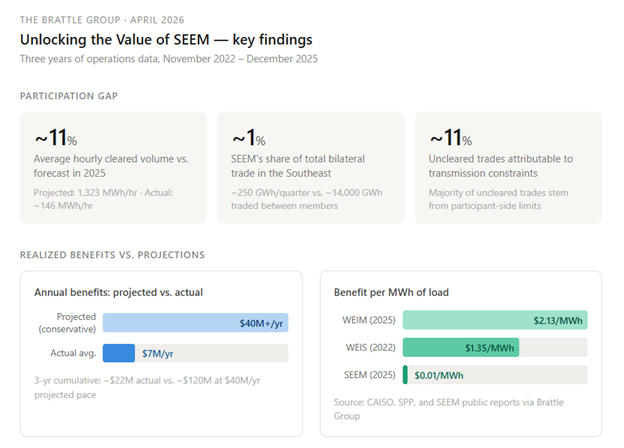

A recent independent analysis from The Brattle Group, prepared for the WRI Polsky Energy Center, puts hard numbers around the participation gap. When SEEM was proposed, its founding members projected $40 to $60 million in annual benefits based on an independent study that assumed a well-functioning, high-participation market. Three years in, the reality looks different: cumulative benefits through 2025 totaled roughly $22 million — about $7 million per year, well short of even the conservative forecast.

Data visualization by PCI Energy Solutions. Source: The Brattle Group, “Unlocking the Value of SEEM,” April 2026. Read the full report.

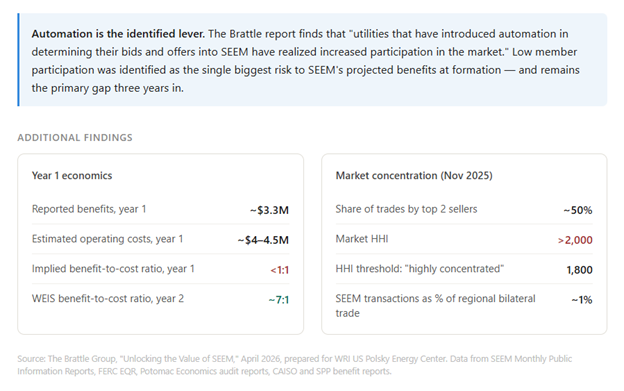

The shortfall isn’t a platform problem. SEEM is functioning as designed. The issue is utilization. Average hourly cleared volumes in 2025 were roughly 11% of the levels originally projected. SEEM transactions account for approximately 1% of total bilateral trade volumes in the Southeast. And in its first year of operation, the market’s roughly $3.3 million in reported benefits likely did not exceed the estimated $4 million annual cost to operate it.

Meanwhile, significant savings sit on the other side of the participation gap. The Brattle report’s market auditor data shows that in a typical month, hundreds of thousands of MWh in bids and offers fall within the cleared price range but never execute — blocked not by transmission constraints (those account for only about 11% of constrained intervals) but by participant-side limitations. The market is ready for more volume. The participants’ workflows often aren’t.

The report identifies automation as a direct lever: utilities that have introduced automated processes for determining their bids and offers into SEEM have realized increased participation. That’s a finding from an independent analyst, not a vendor. It matches what we’ve observed since day one.

Data visualization by PCI Energy Solutions. Source: The Brattle Group, “Unlocking the Value of SEEM,” April 2026. Read the full report.

The SEEM case

SEEM was designed to enable the increased trading volumes necessary for the clean energy transition. Its founding members — utilities, cooperatives, and power producers serving tens of millions of customers across the Southeast — understood that capturing value from a 15-minute market required automation from the start.

PCI SEEMTrader went live on the first day SEEM opened for trading. It’s a cloud-native platform built on top of the GenTrader advanced optimization engine. The formulation and submission of bids and offers can be toggled between fully automatic and manual by a single switch. In the fully automatic mode, PCI SEEMTrader will constantly assess real-time system conditions and constraints to determine the maximum capacity available and its associated costs for trading. It will then apply one of the trader-configured strategies to formulate the bids and offers. Trading strategies allow the trader to set premiums and discounts for offers and bids, respectively. They also allow for withholding certain amounts of capacity from participation in the market. The bids and offers are formulated and submitted just seconds before the close of the submission window to ensure that they reflect the most up to date information. This process takes place every 15 minutes, 24/7 around the clock. The results from the earliest adopters were immediate. Participants who had previously submitted bids manually reported trading at volumes that simply weren’t achievable through a human-paced workflow.

One SEEM founding member reported executing 50 to 100 times the trading volume after moving from manual to autonomous participation. The volume ceiling wasn’t a function of the portfolio. It was a function of the workflow. Remove the workflow constraint and the portfolio’s actual capacity becomes accessible.

That experience aligns with what the Brattle analysis found across the broader market: the single biggest risk to SEEM’s projected benefits was always low member participation, and automation is the most direct lever for closing the gap.

A broader pattern

SEEM is one market. But the underlying dynamic — and the scale of unrealized value — extends well beyond it.

The Brattle report benchmarks SEEM against more coordinated market structures in the western U.S. The Western Energy Imbalance Market (WEIM), which also uses available non-firm transmission for real-time optimization, has delivered nearly $8 billion in cumulative customer savings since 2014. Even the smaller Western Energy Imbalance Service (WEIS) produced a benefit-to-cost ratio of nearly 7:1 in its second year. SEEM’s comparable ratio in its first year was below 1:1.

The comparison isn’t entirely apples to apples — WEIM and WEIS use centralized dispatch, which SEEM does not. But the lesson is directional: markets designed for high-frequency participation reward high-frequency participation. Participants who show up every interval, with precision, capture value that participants who show up intermittently cannot.

As more markets move toward shorter intervals and higher participation frequency, the gap between manual and automated workflows widens. The question for any participant in these markets isn’t whether automation provides an advantage. It’s how much participation and how much value is being left behind by not having it.

The right answer to a machine-speed market is machine-speed trading, with the right human judgment applied at the right moments.

PCI SEEMTrader is purpose-built for autonomous trading in SEEM. To learn more, contact us at [email protected] or visit pcienergysolutions.com.

For a deeper look at the participation gap and the path to unlocking SEEM’s full potential, read The Brattle Group’s report “Unlocking the Value of SEEM.”